The astounding impact of compound interest, i.e. interest earned on previously accumulated interest, must not be underestimated. Albert Einstein once called it the «eighth wonder of the world», and for Warren Buffett it’s nothing less than the most important factor when investing.

Compound interest offers a textbook example of exponential growth.

As the human species is good with linear thinking, but less so with exponentials, it’s quite difficult to understand how powerful this effect is. In case it’s been some time since you darkened the door of a maths classroom: exponential growth involves a particular quantity repeatedly being multiplied by the same factor.

A practical example:

The effect of compound interest on an investment of 10’000 CHF for 30 years at an interest rate of 5%:

Can you see how the total amount doesn’t increase in a linear manner, but exponentially? This is exactly what experts call «compound interest».

After 30 years, the original deposit of 10’000 CHF has now turned into the tidy little sum of 43’219 CHF. So, the interest component amounts to 33’219 CHF. It simply takes your breath away…

What does compound interest have to do with equities?

There can definitely be a link between the two, as the compound interest effect can also be achieved by investing in equities. All you have to do is reinvest the annual increases in value (i.e. price gains) and any dividends. The following example shows that small differences in returns can have massive effects.

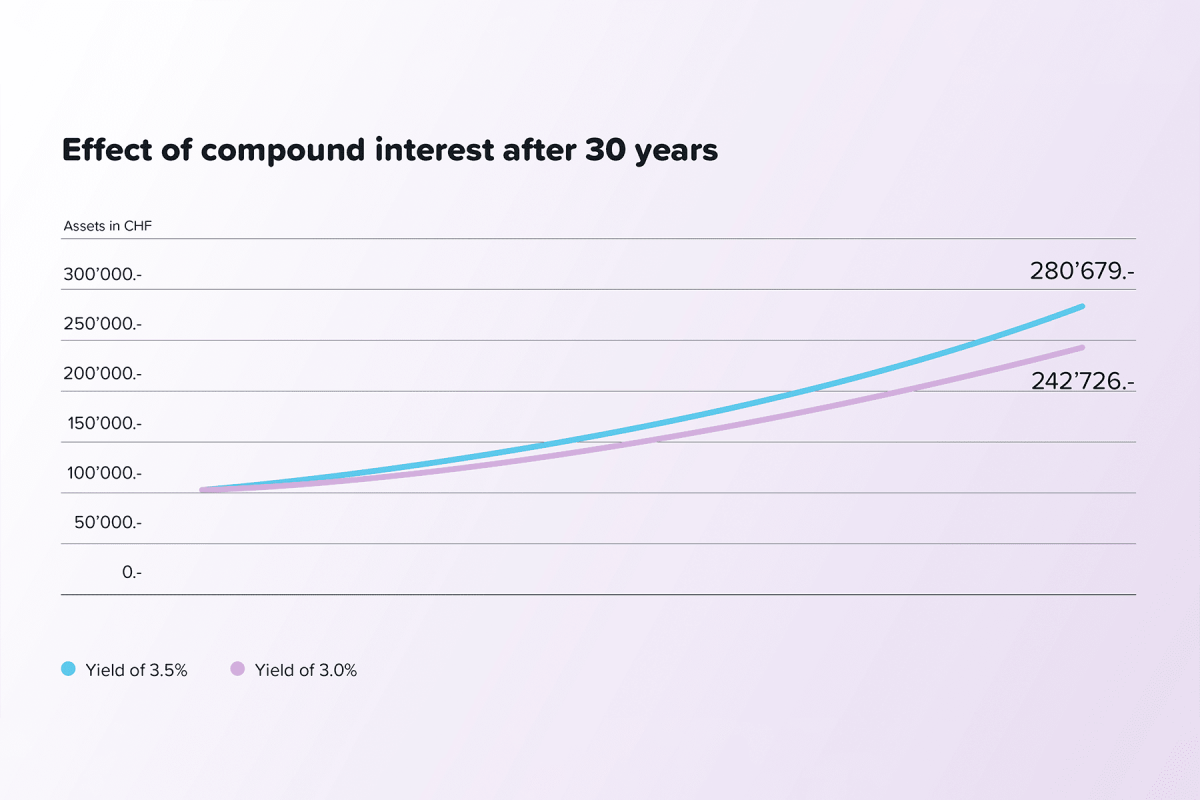

Equity investment of 100’000 CHF invested over 30 years:

With a return of 3.50%: total final value = 280’679 CHF

With a return of 3.00%: total final value = 242’726 CHF

With a return of 3.00%: total final value = 242’726 CHF

The return is dependent on a variety of factors, including the investment strategy chosen. Use the Yuh pillar 3a pension ready reckoner to find out how much money the various investment scenarios could generate for you in retirement.

And what about fees?

We can answer this question, too: it goes without saying that the effect also applies to fees. Small differences in fees can snowball into a major impact over the years. If you can save as little as 0.50% on total fees every year, you’ll have significantly more in your pot at the end. Let’s assume you invest an equity portfolio with a starting value of 100’000 CHF for 30 years. If total fees only amount to 0.50% (as is the case for Yuh) as opposed to 1.00%, you’ll end up with 280’679 CHF rather than 242’726 CHF, assuming an anticipated return of 4.00%. Here too, this means a hefty bonus of around 38’000 CHF.